Table Of Content

The down payment directly reduces the amount of money you need to borrow for the home purchase. Coming up with a down payment can be the hardest part of buying a home—particularly for first-time buyers. Though it makes financial sense to go with a down payment of at least 20%, it’s not always possible to save that much once you realize you’re ready to buy a house and need a place to live. Miranda Crace is a Senior Section Editor for the Rocket Companies, bringing a wealth of knowledge about mortgages, personal finance, real estate, and personal loans for over 10 years. Miranda is dedicated to advancing financial literacy and empowering individuals to achieve their financial and homeownership goals.

First-Time Home Buyers And Down Payments: 73% Of Buyers Put Down Less Than You Think

Deposit products and related services are offered by JPMorgan Chase Bank, N.A. Member FDIC. Make purchases with your debit card, and bank from almost anywhere by phone, tablet or computer and more than 15,000 ATMs and more than 4,700 branches. Further, putting 20% down on your home when you purchase can help show the bank — and yourself — that you're financially ready to purchase a house. Traditionally, a mortgage down payment is at least 5% of a home's sale price.

Use the Home Price

If a buyer put 10-20% down, they may be more committed to the home and less likely to default. If there is more equity in the property, the lender is more likely able to recover its loss in the event of foreclosure. A demand for smaller homes has driven growth in UK property prices early in 2024, according to research by Halifax. But the universal uptick in mortgage costs has been less pronounced in other parts of the UK, with the North East seeing a £2,350 increase.

Calculate mortgage rates

Down Payment on a House: How Much Do You Really Need? - NerdWallet

Down Payment on a House: How Much Do You Really Need?.

Posted: Fri, 12 Apr 2024 07:00:00 GMT [source]

First-time home buyers, at a median age of 35, put down a little less than repeat buyers. At a median age of 59, repeat buyers have had more time to build wealth and home equity. When a loan exceeds a certain amount (the conforming loan limit), it's not insured by the Federal government.

Comparing your mortgage options to lenders with no or low down payments can help you find the most affordable choice. Two potential reasons for the higher median deposit are that buyers have more purchasing power and also want a lower monthly payment due to higher mortgage rates. In 2023, the median percent down payment for all home buyers was 15%, according to the 2023 Profile of Home Buyers and Sellers from the National Association of Realtors.

But do these beliefs match up with what first-time home buyers actually put down to buy a home? Redfin’s study compared median monthly mortgage payments in October 2022 and October 2021, and considered an affordable monthly payment to be no more than 30% of the home buyer’s income. Buying a house that requires immediate repairs will increase these costs. Before buying a home, make sure you know what expenses you’re getting into and that your savings account has enough money to cover them in addition to the down payment and closing costs. Buyers seeking a conventional mortgage loan with low down payments will likely require PMI - more formally known as private mortgage insurance.

Outlooks and past performance are not guarantees of future results. For more information on available products and services, and to discuss your options, please contact a Chase Home Lending Advisor. VA loans are funded by a lender and guaranteed by the Department of Veterans Affairs.

More student loan forgiveness available, but April 30 deadline looms

You might need to look for a loan option that allows a smaller down payment, or you might want to give yourself more time to save up for a larger down payment on a house. Your credit score impacts on your loan and interest rate options. Buyers with credit scores as low as 500 might still be able to get a loan for a home, but they'll likely face higher interest rates and have fewer options. Unlike a fixed-rate loan, an adjustable-rate mortgage has an interest rate that can go up or down based on market conditions. The down payment for an ARM is typically between 3 and 20% and will require PMI for buyers who put down less than 20%. "As interest rates have stabilised and buyers adjust to the new economic reality of owning a home, one way to compensate for higher borrowing costs is to target smaller properties.

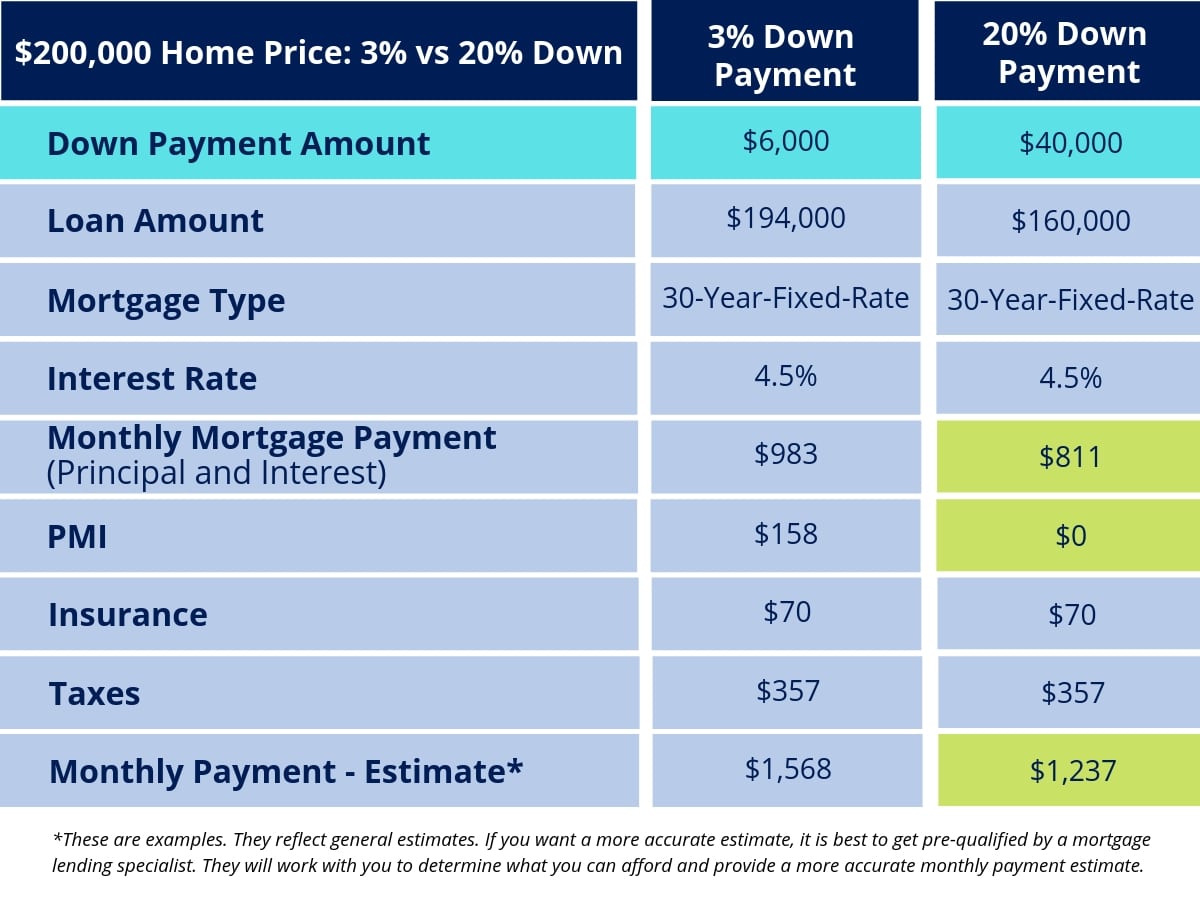

Sometimes you will still need to fund part of the down payment yourself, but you might only need to come up with 1% or 2% of the purchase price instead of 3% or more. If you got a mortgage for 100% of the purchase price, your down payment would be 0%. If you got a mortgage for 80% of the purchase price, your down payment would be 20%. Note that mortgage insurance on FHA loans is applied differently and can be more difficult to get rid of without refinancing. Mortgage lenders require a down payment as protection against a borrower defaulting. The larger your down payment, the less you have to borrow, the lower your payment may be, and the more likely you are to qualify for favorable terms.

The goal of the programs – typically administered by government agencies or private organizations – is to make buying a home attainable. In San Francisco, the salary needed to buy a median-priced home soared to more than $402,000 and, in San Jose, a salary of more than $363,000 was needed to make the monthly mortgage payments. In Anaheim, home buyers needed about $254,000 a year, followed by Oakland, with a required salary of $247,559, and Los Angeles. Once you request a mortgage with a down payment lower than 20%, the lender will arrange PMI with an insurance broker and layer the insurance cost into the transaction. Buyers can either pay a monthly premium for the insurance or a one-time upfront premium when a deal closes. Some lenders provide conventional loans and will not require PMI, but the interest rate may vary as a result.

If a smaller down payment is more reasonable for your budget, you have options. Get expert tips, strategies, news and everything else you need to maximize your money, right to your inbox. If you do make a smaller down payment, keep in mind you'll start out with less equity in your home. Below, CNBC Select looks at where the 20% recommendation came from, how big your down payment really needs to be and more. With all of this in mind, you can determine what size down payment makes sense for you. Equity refers to the difference between the amount you owe on your mortgage and how much your home is worth.

These funds can come from your savings, a gift from family or a friend, proceeds from the sale of another home, grants and other sources. The lender views your down payment as a buyer’s participation in the purchase, and the higher the down payment is, the less risky it is for the lender. Ideally buyers would be able to put down at least 20% of the home price to avoid paying private mortgage insurance, but it’s not a requirement. With the median home price in 2023 at over $425,000, the average homebuyer would need $85,000 just for the down payment. A 20% down payment would keep many home buyers locked out of the housing market. Fortunately, 20% is no longer the benchmark for a down payment on a house.